Oil futures prices decline, fears of oversupply

Oil prices declined in early Asian trade on Tuesday as concerns over crude oil and fuel oil are expected to oversupply, expected cuts in US shale production and is likely to bring a positive impact in US crude stockpiles.

Crude oil prices fell more than 1 percent in the previous session as concerns about potential supply disruptions eased after the coup Friday in Turkey.

US crude, known as West Texas Intermediate (WTI), fell 13 cents to $ 45.11 a barrel after settling down 71 cents, or about 1.6 percent, in the previous session.

Brent crude fell 9 cents to $ 46.87 a barrel after finishing the previous session down 65 cents, or 1.4 percent.

“Oil prices fell due to concerns over supply disruptions in Turkey eased. Crude continues to flow through Turkey without a hitch after the failed coup, according to Minister of Energy states,” ANZ said in a note on Tuesday.

“Energy prices will continue to weigh complex weak broader in the coming days. However, the impact of supply disruptions in several markets are still expected to limit the downside,” he added notes.

fuel inventories in the United States, Europe and Asia are full even though the peak season is expected to fall in the summer, leading traders to store diesel in tankers at sea amid withering demand growth tapered and crude oil production.

However, US oil production is expected to fall in August for the tenth month – 99,000 barrels per day to 4.55 million barrels per day, according to (EIA) reported drilling productivity of the US Energy Information Administration released on Monday.

Further weighing on supply, US commercial crude oil inventories probably fell 2.2 million barrels from 521.8 million barrels in the week ended July 15 early Reuters poll of analysts showed on Monday.

That would be nine consecutive weeks the stock has fallen.

The poll was taken ahead of weekly inventory report from industry group the American Petroleum Institute (API), which will release a report of its shares on Tuesday, and the US Department of Energy’s Energy Information Administration (EIA), which will publish inventory data on Wednesday.

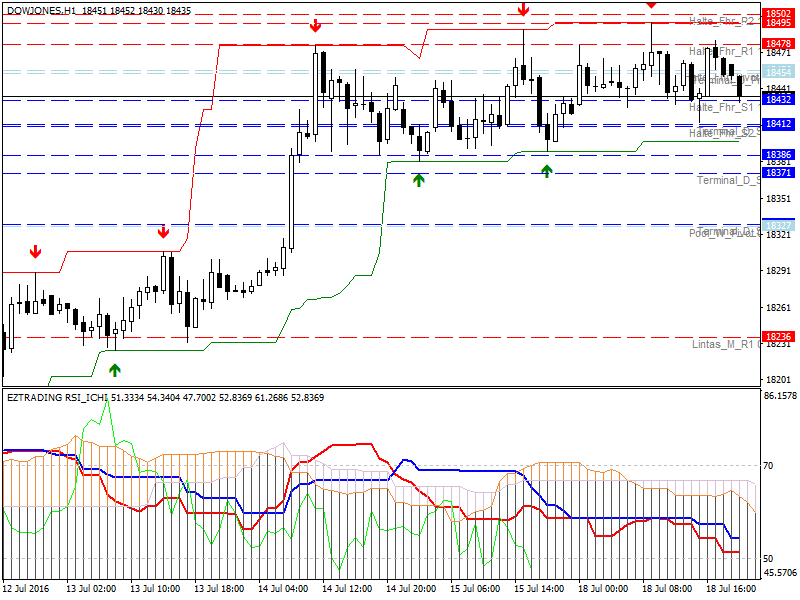

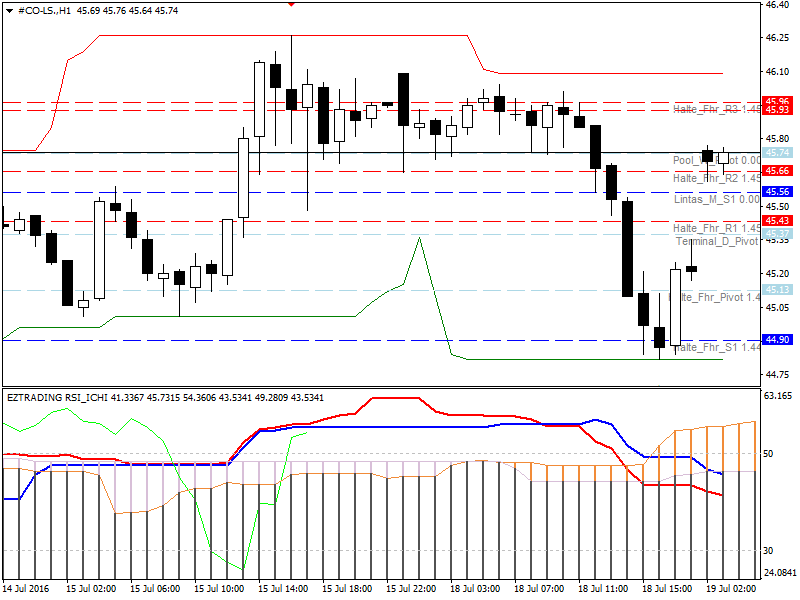

Technically

Resistance: 45.74 45.93 49.98 High / Low: 46.28 / 44.83

Support: 45.66 45.43 45.13 Running Price: 45.70

Comment: For intraday trade today suggest Sell 45.47; stop loss at 46.67; target at 44.87.

The yen weakened on BOJ policy easing expectations

Price yen steady near its lowest point in trading on Tuesday this was due to expectations of monetary policy easing by the Bank of Japan, as well as recovery of risk and speculation about M & A related selling yen.

The New Zealand dollar was one of the big movers in early Asian trade, the kiwi fell sharply after the Reserve Bank of New Zealand increased efforts to impose fresh restrictions on the hot housing market – a move seen as increasing the possibility of rate cuts.

The yen traded at ¥ 106.20 against the dollar, after falling to as low as 106.33 in early trade, its lowest level since June 24.

It is currently supported on the moving average 55-day at 106.34 but a breakthrough level that could encourage traders to test its June 24th low 106.875.

Speculators have been betting that the Bank of Japan will further facilitate the review of the policy in the rate on July 29, as the government in Tokyo to prepare a new fiscal stimulus to boost the economy.

Traders are also unwinding their safe-haven bid in yen due to the initial shock of the last month by Britain to leave the EU and downs, with US stocks hit record highs partly because Brexit has helped to overturn expectations near-term rate hike by the US Federal Reserve.

Traders also expect the yen selling from Softbank (T: 9984), which will purchase the most valuable technology company ARM English (L: ARM) for $ 32 billion in cash.

The British pound rose to ¥ 140.77 (GBPJPY = R), having recovered about nine percent of the low 3 1/2 years ¥ 129.05 hit in the wake of the EU referendum.

Pound steady against most other currencies and traded at $ 1.3266.

The British pound also gained support after Bank of England policy maker Martin Weale said on Monday there was no urgent need to cut interest rates.

The euro stood little changed at $ 1.1076 ahead of the European Central Bank’s policy meeting on Thursday.

While the ECB is widely expected to keep interest rates, some bond traders speculated the central bank may need to overcome the scarcity of bonds that can be bought, with more than half of the German bond is now not eligible to purchase the asset.

The dollar index found support reasonable but lacked momentum to test a four-month high last week marked.

Index (DXY) <= USD> stood at 96.58, below its July 11 high 96.793.

“Although the US payrolls data published earlier this month is strong enough, some US data released after the referendum England showed some weaknesses. The market will be looking for data that will come to see the strength of payrolls data will be sustainable,” said Shinichiro Kadota, chief FX strategist at Barclays (LON: BARC) Japan Securities.

Elsewhere, the New Zealand dollar fell more than one percent after the country’s central bank on Tuesday presented proposed changes to the existing rules of mortgage lending to curb the current boom in house prices.

Kiwi fell to $ 0.7027, its lowest level in three weeks, as the measure was seen as increasing the possibility of a rate cut next month.

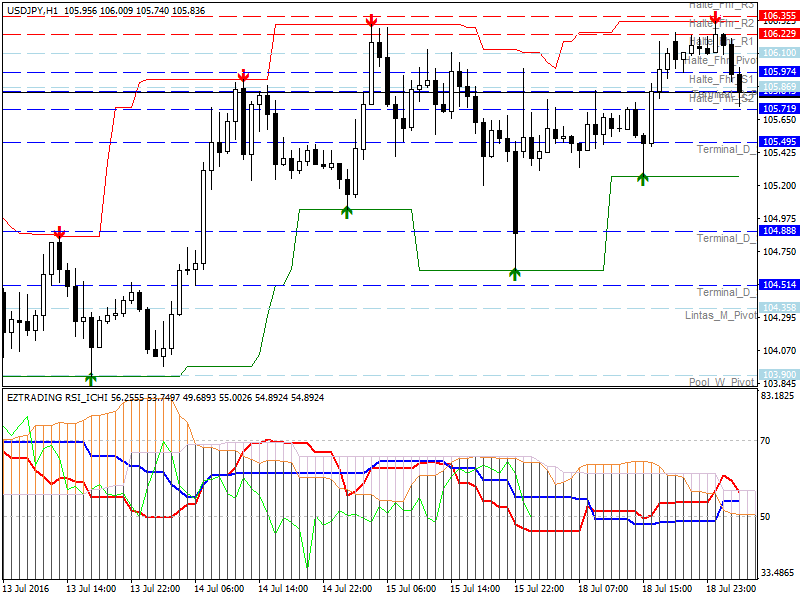

Technically

Resistance: 105.63 105.92 105.95 High / Low: 106.31 / 104.56

Support: Running 104.59 104.93 105.26 Price: 105.84

Comment: For intraday trade today suggest Sell at 105.68; stop loss at 106.28; target at 104.48.

Wall Street on a positive trend – rose to the highest in a week

Stocks reached its highest price point is seen at Tuesday’s trading with the results of the quarter Bank of America raised the confidence of investors look at profit or issuers.

The Dow Jones Industrial Average finished about 15 points higher, with shares of Goldman Sachs and Home Depot contribute the most in profits. The blue-chip index extending its winning streak to seven days, with the fifth consecutive record closing highs.

The S & P 500 also ended up about a quarter percent at a record high, led by the information technology sector and consumer discretionary.

Following Citigroup and JPMorgan Chase last week, Bank of America today as the third major US financial institutions increased second-quarter earnings forecast.

Bank of America beat expectations on earnings and revenue Street Monday, with earnings per share of 36 cents versus 33 cents expected, according to consensus estimates from Thomson Reuters.

Hasbro also beat consensus estimates, and Netflix reported earnings better than expected after the close, but misses the company’s own projections. IBM beat analyst expectations with earnings per share of $ 2.95 compared to the consensus estimate of $ 2.89, according to Thomson Reuters.

The energy sector is the biggest obstacle on the S & P because of rising crude oil inventories triggered investor fears will be a glut of supply, Reuters reported.

In deal news, Japan’s Softbank announced the all-cash bid for the chip designer ARM. This acquisition marks the largest takeover of a British company since June after Brexit decision.

Market Vectors Semiconductor ETF closed 2.9 percent higher after the deal, reached an all-time high back to 2011. This is a positive day eighth best ETF in the nine days since May 20th.

Pan-European STOXX 600 closed slightly higher, helped by the acquisition of ARM Softbank. London-listed shares of ARM jumped more than 40 percent after the announcement Monday. The U.K. The FTSE 100 was also helped by the deal, and closed at 11-month high, according to Reuters.

On the data front, US homebuilder sentiment fell 1 point in July, as the traffic of potential buyers thinning and continued development constraints, according to the monthly reading of builder confidence from the National Association of Home Builders.

Chinese house prices slowed for the second consecutive month in June, especially in small towns, adding fears that the economic rebound may not be sustainable development, according to data from the National Bureau of Statistics of China.

The US dollar edged down against the Turkish lira and mostly flat against a basket of currencies. The euro traded slightly higher against the dollar on Monday, at $ 1.11 while the dollar edged up against the yen, at ¥ 106.14.

The British pound rose half a percent to $ 1.33 after Bank of England policy member Martin Weale said he was not convinced of the need for a rate cut in August. Hawkish statement at odds with many colleagues Weale who said a rate cut possibility, citing expectations that Britain could slip into recession, Reuters reported.

In the US, tension was high after three police officers were killed by a gunman in Baton Rouge on Sunday.

Republican National Convention begins in Cleveland on Monday. Prudential Krosby said, the market will not benefit from a protest about the event or what “created uncertainty”.

US Treasury bond rose slightly Monday. Surta debt benchmark 10-year Treasury moved higher to yield 1.58 percent. Thirty year bonds yield 2.29 percent. Bond prices move inversely to yields.

US crude oil futures settled 71 cents to $ 45.24 a barrel after ending the previous session up 27 cents. Brent crude oil futures settled 1.37 percent at $ 46.96 per barrel.

The Dow Jones Industrial Average closed at a record high of 18,533.05, up 0.09 percent. Shares of DuPont and Home Depot led the gainers, while shares of Travelers is the largest underdeveloped.

The S & P 500 closed at a new record of 2,166.89, up 0.25 percent. Sectors of information technology and consumer discretionary rose the most, while the energy sector and the telecommunications sector led five lower. Consumer staples sector reached a new intraday another all time high Monday, but closed slightly negative.

The Nasdaq index ended 0.52 percent higher to its highest close at 5,055.78 yearly.

Technically

Resistance: 18454 18456 18 478 High / Low: 18490/18233

Support: 18412 18408 18386 Running Price: 18 432

Comment: For intraday trade today suggest Sell at 18416; stop loss at 18476; target at 18 296.